In today’s world, the cost of healthcare is rapidly increasing, making it essential for families to have a reliable safety net. Family health insurance plans provide this much-needed protection. These plans allow families to access necessary medical services without worrying about the financial burden that typically comes with healthcare. In this comprehensive guide, we’ll explore everything you need to know about family health insurance plans: what they are, how they work, their benefits, how premiums are calculated, and more.

What Are Family Health Insurance Plans?

A family health insurance plan is a type of health policy that covers all members of the family, including the policyholder, spouse, children, and sometimes even senior parents or in-laws. Instead of purchasing separate health insurance policies for each individual, a family plan consolidates the coverage under one policy. The coverage amount, known as the sum insured, is shared among the family members, which means that all the members collectively benefit from the coverage.

This approach simplifies the process of managing insurance, as it only requires one policy and premium payment. It also generally proves more economical than buying individual policies for each family member. However, the total coverage amount is divided among all the family members, so if one member has a major medical expense, it can affect the remaining coverage for the other members.

Who Can Be Covered Under Family Health Insurance Plans?

Family health insurance plans typically cover the following members:

- Policyholder: The primary individual purchasing the insurance.

- Spouse: The husband or wife of the policyholder.

- Children: Dependent children, typically up to a certain age, which varies between insurers.

- Senior Parents: Some plans allow you to include your elderly parents, although this may require an additional premium or be available as an add‑on.

Some policies also allow the inclusion of in‑laws, although this is more common in comprehensive family floater plans.

Key Features of Family Health Insurance Plans

One of the main advantages of family health insurance plans is the wide range of coverage they offer. These plans cover a variety of medical needs that families are likely to encounter, including hospitalization, surgery, maternity, and more. Many plans also include cashless hospitalization at network hospitals, which means that the insured doesn’t need to pay upfront for medical expenses; the insurer settles the bills directly with the hospital.

Additionally, most plans cover both pre-hospitalization and post-hospitalization expenses, which can range from doctor’s visits to necessary treatments received before or after hospitalization. The duration of coverage for these expenses can vary, but typically, it’s between 30 and 60 days.

Benefits of Family Health Insurance Plans

Family health insurance plans offer numerous benefits to policyholders. First and foremost, they ensure that your family is protected from unexpected medical costs. Healthcare can be extremely expensive, and even a small medical procedure can lead to significant financial strain. A family plan helps mitigate this risk by covering the cost of medical treatments, allowing you to focus on getting better rather than worrying about medical bills.

Another key benefit is lower premiums. Because family health insurance plans cover multiple members under a single policy, the cost of premiums is generally lower compared to purchasing individual health plans for each family member. This makes it an affordable option for families looking to get comprehensive coverage without breaking the bank.

Additionally, family health plans streamline the process of managing healthcare. Instead of keeping track of multiple policies, you only need to manage one policy, pay one premium, and deal with one claims process. This reduces administrative hassles and helps families stay organized.

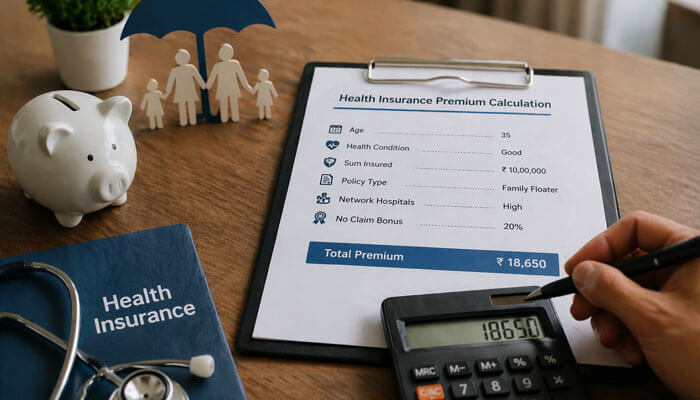

How Premiums Are Calculated

Premiums for family health insurance plans are determined by various factors, including the age of family members, the sum insured, and the medical history of the individuals being covered. The premium will generally increase with the age of the policyholder and the insured family members. Older individuals typically pose a higher risk to insurers, which translates into higher premiums.

The total coverage amount, or sum insured, is another significant factor in determining premiums. Higher coverage limits will naturally result in higher premiums. Other factors that can influence premiums include the location of the policyholder, as healthcare costs vary by region, and the inclusion of additional riders or add‑ons like maternity coverage or critical illness coverage.

Types of Family Health Insurance Plans

There are various types of family health insurance plans available, and the right choice depends on your family’s specific needs.

- Family Floater Plans: This is the most common type of family health insurance plan. The sum insured is shared among all family members, and it’s ideal for younger families or families where members have similar health needs.

- Individual Cover for Each Member: In this plan, each family member has a separate sum insured. While this can lead to higher premiums, it may be beneficial for families with members who have different healthcare needs, such as older individuals or those with pre‑existing conditions.

- Senior Citizen Family Plans: Designed specifically for families with elderly members, these plans usually offer coverage for critical illnesses, extended hospitalization, and other healthcare services that older adults may need.

- Critical Illness + Family Health Combo: Some insurers offer policies that combine coverage for regular medical needs and critical illnesses like cancer, heart attack, and stroke. These plans are ideal for families looking for enhanced protection.

Choosing the Right Family Health Insurance Plan

Selecting the right family health insurance plan requires careful consideration of several factors:

- Evaluate the Health Needs of All Family Members: Consider the age, medical history, and healthcare requirements of each member before making a decision.

- Check Network Hospitals: Ensure the insurer has a wide network of hospitals and clinics in your area. The larger the network, the easier it will be to access cashless services.

- Choose an Adequate Sum Insured: Your sum insured should be sufficient to cover the healthcare expenses of all family members. A general rule of thumb is to select a sum insured that is 3 to 4 times your family’s annual medical expenses.

- Look for Add‑ons: If your family has specific health needs, look for add‑ons like maternity coverage, dental treatment, or coverage for pre‑existing conditions.

- Understand the Claim Process: Ensure that the insurer has a smooth and fast claim process. The quicker and easier the claims process, the better the overall experience will be in the event of a medical emergency.

Conclusion

A family health insurance plan is a critical component of financial planning for families. It provides financial security and peace of mind, knowing that your family is protected in times of illness or injury. By choosing the right plan and understanding its features, you can ensure that your family has access to quality healthcare without breaking the bank.

As healthcare costs continue to rise, securing a comprehensive family health insurance plan is one of the best ways to ensure that you and your loved ones are well taken care of in times of need.